Guyana Subsea Titanium Order: How $63.5M Reprices 25-Year Service Life

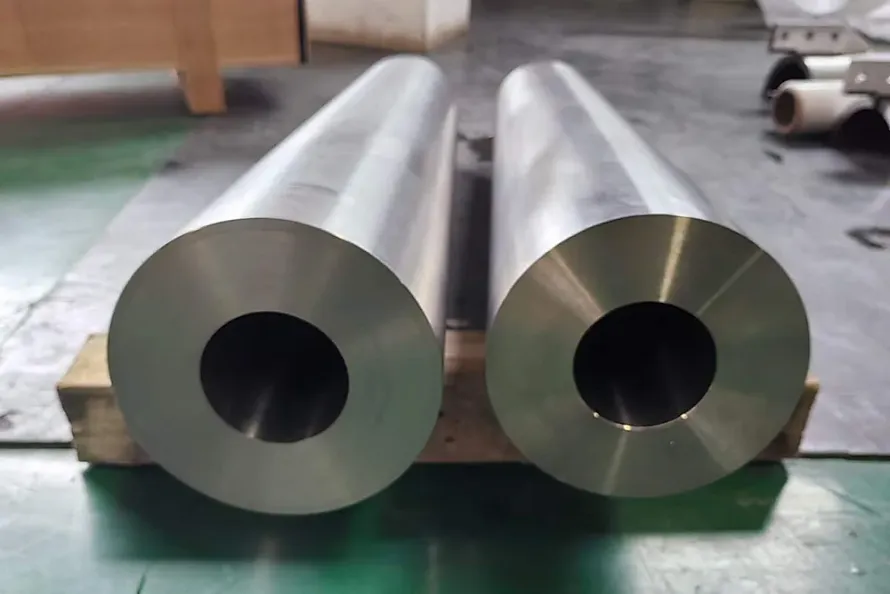

On April 7, Hunting PLC announced a $63.5 million titanium stress joint order tied to ExxonMobil's FPSO program in the Guyana basin. The titanium alloy stress joints will sit at the top of a steel catenary riser (SCR) system. It is the largest single subsea titanium order booked so far in 2026. The order itself is not revolutionary — but it pulls a question that has been parked for eight years back onto the table: does subsea titanium's 25-year life-cycle economics actually pencil out at $60 oil? Why this order is worth unpackingSet the background first. An FPSO (Floating Production Storage and Offloading) riser system is the umbilical that ferries production from a deepwater wellhead up to the floating platform. At 2,000+ m water depth, the riser carries three load sets: gravity-driven self-weight, vortex-induced vibration (VIV) from current, and bending fatigue induced by platform drift. The fatigue-life bottleneck sits at the stress joint where the riser meets the floating platform. Conventional steel stress joints in that position are designed for 12–15 years of service. FPSO programs themselves are routinely designed for 25. That gap is exactly what titanium alloy stress joints solve. Titanium (4.51 g/cm³) is 42% lighter than steel (7.85 g/cm³), with higher specific strength and far better seawater corrosion resistance. It pushes bending fatigue life out to 25–30 years, with no mid-life replacement. On a life-cycle cost basis, the titanium joint is 5–8 times the upfront cost of steel — but it eliminates a mid-life intervention. In deepwater, a mid-life intervention means partial FPSO shut-in plus heavy-vessel mobilization, and the unit cost runs into the tens of millions per event. What does Hunting's $63.5M order actually contain? Reverse-engineered against an industry average of $350–500/kg, the order represents 130–180 tonnes of titanium thick-wall pipe and forged stock — concentrated in Ti-6Al-4V Gr.5 or Pd-microalloyed Gr.7. The Guyana basin is ExxonMobil's flagship deepwater play and the fastest-growing deepwater basin in the world. Production passed 650,000 bbl/day in 2025, with 1.3 million bbl/day planned for 2027. Every FPSO in that ramp needs a titanium riser package on the same scale. This is the start of an order curve, not the peak. The arithmetic of 25-year life Lay the 25-year economics out in full and titanium stops looking like a luxury material. It reads as the NPV-optimal answer. Steel SCR route: $8M upfront capex + $45M mid-life replacement campaign at year 12–15 (downtime + heavy-lift vessel + redeployment) + decommissioning at year 25. Total life-cycle cost: ~$53M, with a non-trivial mid-life production-loss exposure layered on top. Titanium stress joint route: $55M upfront capex + decommissioning at year 25. Total life-cycle cost: $55M, no mid-life downtime exposure, and the FPSO runs at full availability across the entire 25-year window. Both totals land in the same range. But the risk shape is different — the titanium joint converts an uncertain mid-life intervention cost (plus a time-risk premium) into a fixed upfront capex line. At $60 oil, with deepwater production cadences tight, that is the trade an ExxonMobil-class operator wants to make. The relevant context: subsea titanium risers were largely shelved over the past eight years because $30–50 oil broke the project NPV — the titanium upfront premium ate the internal rate of return. Since 2025, with the price deck back to $60–70 and deepwater production re-entering an expansion cycle, the math has flipped positive again. The Hunting order is the first industrial-scale evidence that the new math holds. Gr.7 micro-alloyed supply: a very short list Titanium stress joints are not built from off-the-shelf Gr.5 forgings. Subsea risers in long-term seawater contact demand exceptional resistance to crevice corrosion and stress corrosion cracking (SCC). The standard answer is Pd-micro-alloyed Gr.7 or Gr.12 — adding 0.12–0.25% Pd, or 0.3% Mo+Ni, shifts the corrosion potential toward the noble end of the seawater curve. Global supply on these grades is narrow. Fewer than 15 mills worldwide can deliver Gr.7 thick-wall welded pipe and large-section forgings. Far fewer hold the offshore certifications — DNV, ABS, API 17R — required to put the part on a real FPSO. Inside China, the count of mills with stable Gr.7/Gr.12 offshore-grade supply is in the single digits, and NORSOK/DNV qualification audits commonly take 18 months. Our Baoji spot inventory system shows 20 tonnes of Gr.7/Gr.12 titanium pipe and forged stock in April 2026. The size envelope covers OD 89–219 mm thick-wall welded pipe (8–25 mm wall) and 200–500 kg forging classes. Over the past three months, RFQ frequency from offshore and seawater-contact chemical buyers has lifted noticeably. The Hunting Guyana order is the visible tip — in the same window, Petrobras (Brazil), Equinor (Norway), and PETRONAS (Malaysia) all have deepwater expansion programs with titanium stress joint options on the table. A checklist for offshore buyersIf you are scoping titanium riser procurement for 2026–2028 deepwater programs, three actions belong at the top. First, lock the grade route early. Gr.7 fits long-term seawater service joints and flanges. Gr.12 fits higher-temperature mixed seawater + chemical duty. Gr.5 does not belong on long-life seawater parts. The cost of getting this wrong is enormous — switching grade after the part is on the line triggers a full re-review of the FPSO design package. Second, write "NORSOK M-630 + DNV-RP-O501 dual qualification + Pd micro-alloy traceability to melt heat number" into the qualification gate as a hard requirement. Subsea titanium failures are rarely material failures. They are lot-to-lot variance failures that surface as localized corrosion. Traceability matters more than unit price. Third, count spot inventory as a line item in the bid model. Engineering windows on deepwater programs are tightening. In Q1 2026, suppliers with spot-deliverable titanium pipes and titanium tubes closed bids at roughly 22% higher win rates than those quoting from futures runs. Once an order is awarded, the fabrication window is often 14–20 weeks. No spot, no seat at the table. Two curves are about to lift together over the next 12–18 months. One is total order volume returning toward the 2014–2016 peak. The other is Gr.7/Gr.12 availability staying tight. Where those curves cross is the moment titanium risers become the standard option in deepwater oil and gas — not the exotic one. Hunting's $63.5M is the starting point of that curve, not the destination. Related Products & ServicesService → Stocking Programs for Aerospace and Subsea Titanium — spot-backed delivery for offshore programs running on tight engineering windows Product → Titanium Pipes — Gr.7/Gr.12 thick-wall offshore welded pipe, seawater-corrosion grades in stock Product → Titanium Equipment — custom forging capability for subsea stress joints, flanges, and fittingsAbout: Titanium Seller is a supply chain platform based in Baoji, China's Titanium Valley.